Home->Resources->Income Tax->

Option for individuals and HUF for computation of tax as per new tax slab under Section 115BAC

[Updated as on April 27, 2020]

Finance Act 2020 has introduced a new section 115BAC which gives an opportunity to individuals and HUF to opt for payment of tax calculated as per a new tax slab as provided in (1) of the section. This is applicable from assessment year 2021-22 subject to fulfillment of conditions as stipulated in (2) of the section.

Rate of tax shall be as per the following table:

Computation of total income [115BAC(2)]

In computing the total income, the following benefits will not be available:

-

Following deductions/exemptions which are otherwise eligible to an individual or HUF:

2. set off of any loss,

-

carried forward or depreciation from any earlier assessment year, if such loss or depreciation is attributable to any of the deductions referred above;

-

under the head “Income from house property” with any other head of income in the same year;

3. exemption or deduction for allowances or perquisite, by whatever name called, provided under any other law for the time being in force.

Deductions or exemptions other than those mentioned above shall be deducted before arriving at the total income for the purpose of calculation of tax under this section.

Points to note

-

The loss or depreciation as referred in B above namely carried forward loss or depreciation from earlier assessment years attributable to any of the deductions referred in A above and loss on house property, which are not considered in computing the total income shall be deemed to have been given full effect to and no further deduction for such loss or depreciation shall be allowed for any subsequent year.

-

If there is any depreciation allowance in respect of a block of assets which has not been given full effect to as on the beginning of previous year 2020-21, the written down value as on 1st April 2020 of such block of assets shall be modified accordingly if the assessee opts to pay tax under the new scheme for the assessment year 2021-22.

-

In case a person, having a Unit in the International Financial Services Centre, as referred to in sub-section (1A) of section 80LA, which has opted for the new tax scheme, the deduction under section 80LA shall be available to such Unit subject to fulfillment of the conditions contained in the said section. For the purposes, the term “Unit” shall have the meaning assigned to it in clause (zc) of section 2 of the Special Economic Zones Act, 2005.

-

In respect of exemptions on allowances notified under section 10(14), of the Act, the list of the allowances on which exemption shall continue to be available under the new scheme has not yet been published by the department. It is expected that exemptions on following allowances available to the Individual or HUF shall continue under the new scheme:

-

Transport Allowance granted to a divyang employee to meet expenditure for the purpose of commuting between place of residence and place of duty

-

Conveyance Allowance granted to meet the expenditure on conveyance in performance of duties of an office;

-

Any Allowance granted to meet the cost of travel on tour or on transfer;

-

Daily Allowance to meet the ordinary daily charges incurred by an employee on account of absence from his normal place of duty.

Exercise of option

As per 115BAC(5), the assessee shall exercise option in the following manner:

Conditions to be fulfilled:

-

The total income for the purpose of calculation of tax shall be computed strictly in accordance with the provisions of sub section (2). In case a person fails to satisfy the conditions contained in sub-section (2) in any previous year, the option shall become invalid in respect of such previous year and it shall be deemed that no option was exercised. Such option shall also become invalid in respect of subsequent assessment years.

-

The assessee shall be an individual or HUF in order to be eligible for making option under the section.

-

The option is to be exercised within the time period as specified in sub section (5).

Old Scheme Vs New Scheme

On analysis of the tax slab under the old scheme and new scheme, it can be seen that the new scheme appears to be more beneficial as the tax rates are comparatively less for income slabs above Rs.5 lakh. But on the other hand, most of the deductions or exemptions available under the old scheme are disallowed in computing the total income for the purpose of calculation of tax as per the new scheme. Time and again many governments have introduced various deductions in order to compel assessees to make investments on the pretext of reducing tax liability. Recently Government introduced sections 80EE & 80EEA to boost the real estate sector. Deductions date to a very old period and gradually assessees have developed the habit of making regular investments which gives both return as well as savings in tax liability at the same time.

Though new scheme does not give weightage to deductions, the assessees can still make investments and continue in old scheme paying tax lesser than that computed under new scheme. By using mathematical formulae, we can calculate the minimum deduction required to continue in the old scheme and avail tax benefit for various income slabs.

Compution of minimum required deduction

Following variables may be used:

T= Total income before giving effect to the exemptions or deductions ineligible under the new scheme but after adjusting the deductions and exemptions eligible.

D= Value of exemptions or deductions, carried forward losses or depreciation and other benefits ineligible under the new scheme as per sub section (2) but available under the old scheme.

The table below shows the formulae to be applied based on the slab in which the Total income so arrived above falls.

Table showing computation of minimum deduction for various income slabs and corresponding tax under old scheme and new scheme. [All amounts are in Rs]

Selecting the best option

As given in sub section (5), assessees have to make the option either to select the new scheme or to continue in the old scheme. This choice is not so difficult for assessees not having income from business or profession as they can compute the income at the time of filing return both under the new scheme and old scheme and select the most favourable option. But for employees, they have to make the choice at the beginning of the year when asked by the employer for the purpose of deduction of TDS.

In the case of assessees having income from business or profession, the choice has to be made very carefully as there is restriction in reviewing the choice once made. Hence if they wish to forego the deductions to which they are already eligible, it should result in tax savings rather than paying more tax than what was payable if the option was not exercised.

In order to assist in making the optimum choice, an assessee may follow the steps below:

-

Compute the total income for the previous year without giving effect to the exemptions or deductions ineligible under the new scheme but after adjusting the deductions and exemptions eligible.

-

Compute the value of exemptions or deductions, carried forward losses or depreciation and other benefits ineligible under the new scheme as per sub section (2) but available under the old scheme to which the assessee is entitled for the relevant previous year.

-

Calculate the minimum deduction using the formulae given above.

-

If the value in (b) is lesser than the minimum deduction calculated, it will be better to switch to new scheme.

-

Assessee if it wishes to continue in old scheme can make further investment, if possible, beyond the minimum deduction and earn more tax benefit compared to the new scheme.

-

Assessees having income from business or profession should project the above figures for subsequent assessment years also in order to arrive at a decision.

This method employs mathematical formulae merely to support the assessee in making a suitable choice and assessee has to make the judgment considering all relevant factors such as rate of return, fund requirement, avoiding tax complexities, maintenance of records etc.

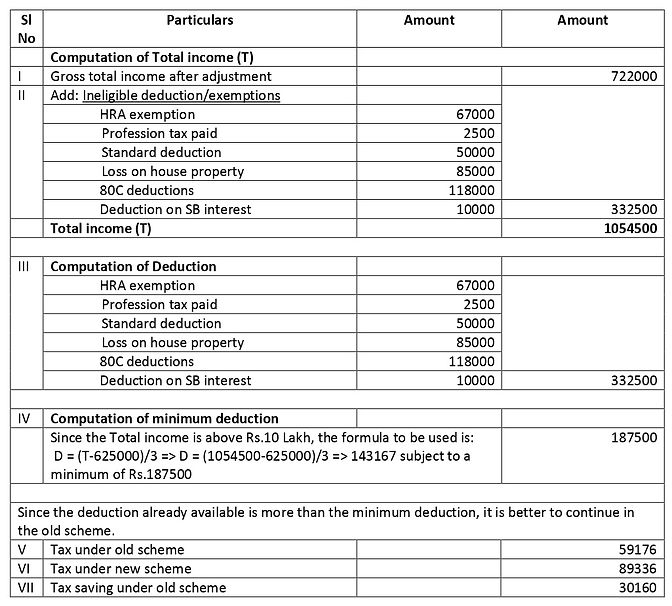

Illustration

-

Amal has arrived at a gross total income of Rs.822000 for the financial year 2020-21. In his computation he has considered the following deductions:

HRA exemption: Rs.67000

Profession tax paid: Rs.2500

Standard deduction: Rs.50000

Loss on house property: Rs.85000

80C deductions: Rs.118000

Deduction on SB interest: Rs.10000

Which would be better option for him?

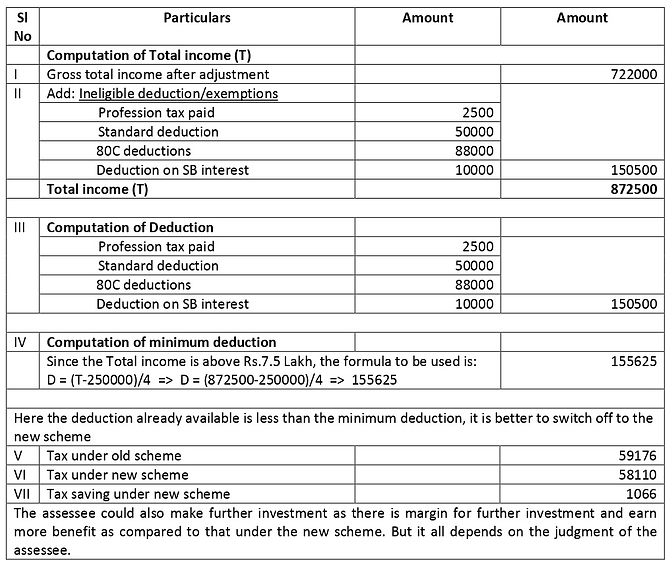

2. Consider in the above example, HRA exemption and loss on house property was not available and deduction under 80C is only Rs.88000.

Page views: