Applicability of GST on Bill to Ship to transactions

[Updated as on April 27, 2020]

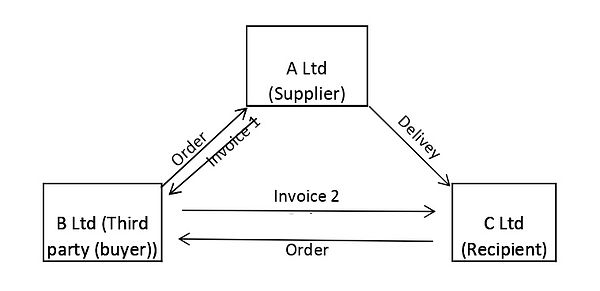

Bill to ship to transaction is a transaction whereby goods are supplied by the Supplier on the request of a third party (buyer) to the recipient of the goods with whom the third party (buyer) has entered into an agreement for supply of goods. Thus there are two separate agreements and two invoices in this transaction i.e one between supplier and third party (buyer) and the other between third party (buyer) and the recipient of the goods. However the movement of goods take place only once i.e between the supplier and the recipient. This can be made clear with the following example:

-

C Ltd enters into agreement with B Ltd for purchase of rice.

-

B Ltd enter in turn enters into agreement with A Ltd for purchase of rice directing it to be delivered directly to C Ltd. Here A Ltd will mention B Ltd as the ‘Billed to’ party and C Ltd as the ‘Shipped to’ party.

Applicability of GST

Bill to Ship to transactions are specifically covered by the provisions of GST. There are specific provisions in order to identify the place of supply in Section 10(1)(b) of the IGST Act. As regards availing of input tax credit, an explanation was added to Section 16(2) of the CGST Act, to enable the third party (buyer) to avail input tax credit even without receiving the goods.

Place of supply

As per Section 10(1)(b) of the IGST Act, where the goods are delivered by the supplier to a recipient or any other person on the direction of a third person, whether acting as an agent or otherwise, before or during movement of goods, either by way of transfer of documents of title to the goods or otherwise, it shall be deemed that the said third person has received the goods and the place of supply of such goods shall be the principal place of business of such person.

Thus in a Bill to Ship to transaction, the place of supply shall be the principal place of business of the person who enters into contract with the supplier and directs delivery of the goods to the recipient of the goods from the premises of the Supplier. In the above example, the place of supply is the principal place of business of B Ltd.

Determination of the place of supply is very important in understanding the nature of the supply and the category of GST to be payable. Supply of goods or services where the location of the supplier and the place of supply are in the same State or same Union territory shall be treated as intra-State supply and is liable to SGST or UTGST. Supply of goods or services, where the location of the supplier and the place of supply are in two different States, two different Union territories or in a State and a Union territory, shall be treated as a supply in the course of inter-State trade or commerce and is liable to IGST.

Consider an example where Z Ltd located in Delhi has contracted with Y Ltd in Delhi for supply of Raw Cashews. Y Ltd immediately entered into a contract with X Ltd in Andhra Pradesh for purchase of raw cashews directing to deliver the same directly to Z Ltd.

Here since two transactions are involved, place of supply has to be identified for both transactions.

1. Between X Ltd and Y Ltd

Since the goods are delivered directly to Z Ltd on the request of the third party (buyer) which is Y Ltd in this case, as per Section 10(1)(b) of the IGST Act, the place of supply is the principal place of business of Y Ltd. Therefore the place of supply for the transaction between X Ltd and Y Ltd is Delhi and since the location of the supplier and the place of supply are in two different States, IGST will be applicable in this case.

2. Between Y Ltd and Z Ltd

Here there is no physical transfer of goods taking place between the premises of both parties. But the value at which goods are sold by X Ltd to Y Ltd and Y Ltd to Z Ltd differs and Y Ltd would add their profit margin on the goods. Y Ltd would therefore issue invoice to Z Ltd for the sale value of the goods and is liable to pay GST on the amount. As per Section 10(1)(a) of the IGST Act, where the supply involves movement of goods, whether by the supplier or the recipient or by any other person, the place of supply of such goods shall be the location of the goods at the time at which the movement of goods terminates for delivery to the recipient. Here the movement of goods terminated for delivery at the premises of the recipient who in this case is Z Ltd and the place of supply is therefore Delhi. Since the location of the supplier and the place of supply are in the same State, CGST & SGST will be applicable in this case.

Issue of invoices

In a Bill to Ship to transactions, as two transactions are involved between three parties, two invoices are to be issued by the concerned parties-

-

By the Supplier- in the transaction between third party (buyer) and the Supplier

-

By the third party (buyer)- in the transaction between third party (buyer) and the recipient.

These parties have to determine the place of supply and charge applicable GST in their invoice

Input tax credit

As per Section 16(2) of the CGST Act, no registered person shall be entitled to the credit of any input tax in respect of any supply of goods or services or both to him unless,––

-

he is in possession of a tax invoice or debit note issued by a supplier registered under this Act, or such other tax paying documents as may be prescribed;

-

he has received the goods or services or both.

Explanation.—For the purposes of this clause, it shall be deemed that the registered person has received the goods where the goods are delivered by the supplier to a recipient or any other person on the direction of such registered person, whether acting as an agent or otherwise, before or during movement of goods, either by way of transfer of documents of title to goods or otherwise;

Based on the above explanation to the section, in a Bill to Ship to transaction, the third party (buyer) can claim input tax credit on the basis of invoice issued by the supplier even though he has not received the goods. The recipient on the other hand can also claim input tax credit based on the invoice issued by the third party (buyer) as they are in receipt of the goods thereby complying with the requirements for availing input tax credit as per the provisions of section 16(2).

E-Way Bill

In a Bill to Ship to transaction, the movement of goods is taking place only once i.e between the Supplier and the recipient of the goods. As per Rule 138 of the CGST Rules, e-Way bill has to be raised by the person who causes movement of goods before commencement of such movement by furnishing information in Part A of FORM GST EWB-01. It is already clear that two invoices are to be issued in case of Bill to Ship to transaction. Hence there is confusion as to who has to raise the e-Way bill and how many are to be generated.

The same has been clarified vide press release issued by CBIC dated 23/04/2018. It was clarified that in a Bill to Ship to transaction, either the Supplier or the third party (buyer) can raise the e-Way bill and only one e-Way Bill is required to be generated as per the following procedure:

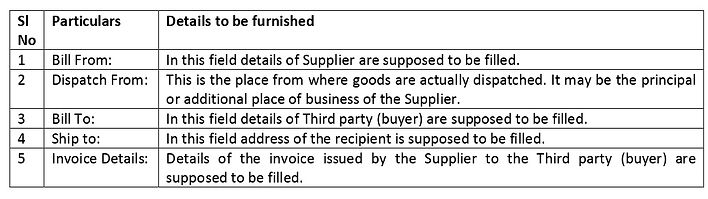

Case -1: Where e-Way Bill is generated by Supplier

The following fields shall be filled in Part A of GST FORM EWB-01:

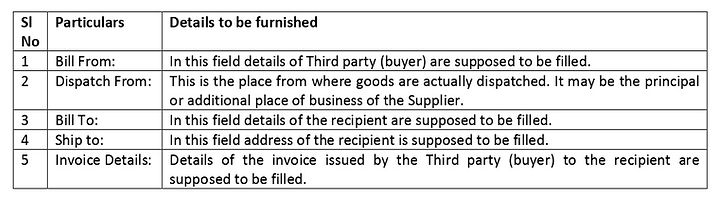

Case -2: Where e-Way Bill is generated by Third party (buyer)

The following fields shall be filled in Part A of GST FORM EWB-01:

Page views: