Taxability of commuted pension

Taxability of commuted pension received by an individual is covered by Section 10(10A) of the Income Tax Act, 1961.

Receipts which are fully exempt [10(10A)(i) & (iii)]

Commutation of pension received is fully exempt in the following cases:

-

Amount received under the Civil Pensions (Commutation) Rules of the Central Government.

-

Amount received under similar scheme applicable to:

-

the members of the civil services of the Union or holders of posts connected with defence or of civil posts under the Union (such members or holders being persons not governed by the said Rules) or

-

to the members of the all-India services or

-

to the members of the defence services or

-

to the members of the civil services of a State or

-

holders of civil posts under a State or

-

to the employees of a local authority or

-

a corporation established by a Central, State or Provincial Act.

-

-

any payment in commutation of pension received from a fund set up under section 10(23AAB) of the Income Tax Act, 1961 by the Life Insurance Corporation of India or any other insurer under a pension scheme to which contribution is made by any person for the purpose of receiving pension from such fund and which is approved by Insurance Regulatory and Development Authority.

Civil services, civil posts and all india services denotes the civil side of administration whereas defence services and posts connected with defence denotes the defense side of administration in the country.

Civil services comprises of civil services of the union and the state. All india services are common to both central and the state and comprises of Indian Administrative service, Indian Police service and Indian Forest service. Civil post means government service other than those services of Union or States which are formally constituted services. All posts hold by the public servants other than the posts in the Defence Forces shall be deemed to be civil posts.

Defence service means established defence services and post connected with defence denotes post which is controlled by the defence side of administration of the country.

Local authority shall mean a municipal committee, district board, body of port Commissioners or other authority legally entitled to, or entrusted by the Government with, the control or management of a municipal or local fund (Section 3(31) of the General Clauses Act, 1897). This includes Municipalities, District Boards, Panchayats, Port Trusts as decided in various judicial decisions.

Where an Act itself establishes a Corporation, it is a Corporation established by the Act. The Act may be a Central, State or Provincial Act. Examples are State Bank of India established by the State Bank of India Act, Life Insurance Corporation established by the Life Insurance Corporation Act.

Summarising, commuted pension received by employees of Central and State governments, local authority and statutory corporation is fully exempt from income tax. Also commuted pension received from pension fund set up by LIC or other insurer approved by IRDA is also fully exempt. There are further exemptions as provided by various circulars as follows:

-

Judges of the Supreme Court and High Courts will be entitled to the exemption of the commuted portion under section 10(10A)(i) of the Act vide Circular No. 623 dated 6-1-1992.

-

Salary received by employees of the UNO or any person covered under the UN (Privileges and Immunities), Act, 1947 and pension received by them from the UN will also be exempt from income-tax as per Circular No. 293 dated 10/02/1981.

-

Lump sum amount received in lieu of pension by persons absorbed in public sector corporations will be fully exempt under 10(10A)(i) as per Circular No. 286 dated 17/11/1980.

Receipts which are partially exempt [10(10A)(ii)]

Commutation of pension received in the following cases is exempt partially:

-

any payment in commutation of pension received under any scheme of any other employer is exempt subject to the limit as follows:

-

where the employee receives any gratuity, the commuted value of one-third of the pension which he is normally entitled to receive, and

-

in any other case, the commuted value of one-half of such pension.

-

The commuted value for this purpose shall be determined having regard to the age of the recipient, the state of his health, the rate of interest and officially recognized tables of mortality.

Consider an example of Mr.Nakul who retired on 31/01/2020 after 40 years of service from a private company. He is entitled to a pension of Rs.30000 of which he commuted 40 percent and received Rs.12 Lakhs.

Exemption shall be computed as follows:

-

If he had received gratuity:

Commuted value of full pension => Rs.1200000*100/40 => Rs.3000000

1/3rd of commuted value => Rs.1000000

Amount of exemption: 1000000

Taxable amount => Rs.200000 [Rs.1200000- Rs.1000000]

-

Other than the case where gratuity is received:

Commuted value of full pension => Rs.1200000*100/40 => Rs.3000000

1/2 of commuted value => Rs.1500000

Amount of exemption: 1500000

Hence no amount is taxable.

The uncommuted amount of Rs.18000 will be taxable.

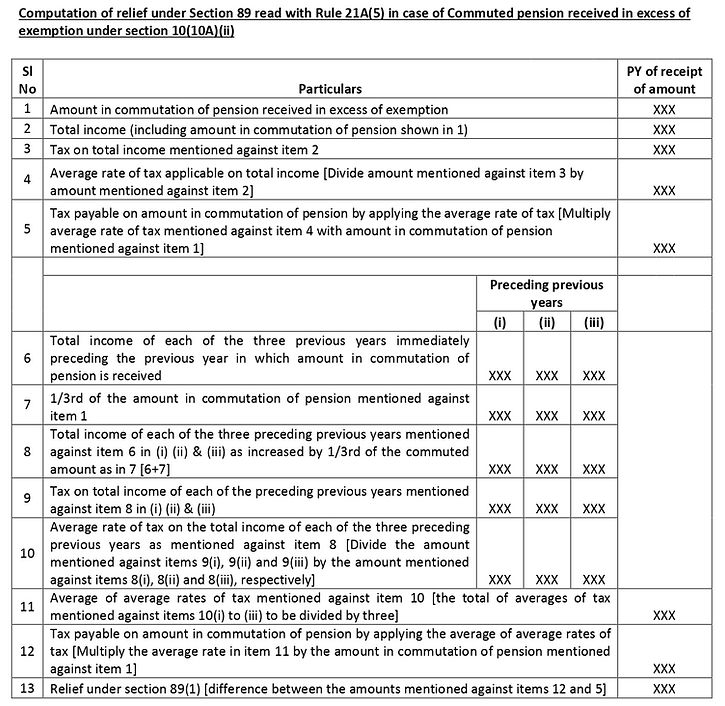

Relief under Section 89

Where the amount received by way of commutation of pension exceeds the amount exempted under this clause, the assessee can claim relief under Section 89 read with Rule 21A(5). The relief shall be calculated as under:

Filing of Form No.10E

Rule 21AA requires that where an assessee, being a Government servant or an employee in a [company, co-operative society, local authority, university, institution, association or body], is entitled to relief under sub-section (1) of section 89, he may furnish to the person responsible for paying any income chargeable under the head "Salaries", the particulars specified in Form No. 10E. Now IT department requires assessees to file this form electronically through the e-filing portal. Form 10E has to be filed electronically where the assessee wishes to claim relief under Section 89.

Illustration

Mr.Ashok retired on 31/08/2019 after 35 years of service from a private firm. He is entitled to a pension of Rs.22500 of which he commuted 40% amount and received Rs.900000 along with gratuity on 25/09/2019. His total income for the FY 2019-20 excluding commuted amount is Rs.750000. Also his total income and tax paid for the FYs 2016-17, 2017-18 & 2018-19 are as follows:

FY Total income Tax paid

2016-17 565000 39140

2017-18 580000 29355

2018-19 675000 49400

Since he had received gratuity, exemption shall be computed as follows:

Commuted value of full pension => Rs.900000/(40%) => Rs.2250000

1/3rd of commuted value => Rs.750000

Amount of exemption: 750000

Taxable amount => Rs.150000 [Rs.900000- Rs.750000]

The taxable amount shall be included in the total income for the previous year in which amount in commutation of pension is received and chargeable to tax accordingly. However he can claim relief under Section 89 as follows:

Page views: