GST on Used Goods

GST provides for special treatment to used or second hand goods being goods used as such or after such minor processing which does not change the nature of the goods. CGST Rules provides for adopting marginal scheme in valuation of supplies. Also purchases made from unregistered suppliers are exempted from applicability of reverse charge mechanism. However special tax rates are not specified for such goods except for used vehicles issued vide a separate notification.

Valuation of second hand goods

Valuation of second hand goods sold by a dealer of such goods

As per Sec 15(1) of CGST Act, 2017, the value of a supply of goods or services or both shall be the transaction value, which is the price actually paid or payable for the said supply of goods or services or both where the supplier and the recipient of the supply are not related and the price is the sole consideration for the supply. However vide sub section (5) to this section, value of certain supplies as may be notified by the Government on the recommendations of the Council shall be determined in such manner as may be prescribed. Accordingly rule 32(5) of CGST Rules 2017 prescribes the manner for determination of taxable value of second hand goods i.e used goods as such or after such minor processing which does not change the nature of the goods and sold by a dealer of such goods.

Valuation as per Rule 32(5)

Value of supply = Selling price – Purchase price

In case the value so arrived is negative, it shall be ignored.

However in case the goods intended to be sold have been repurchased from a defaulting borrower who is not registered, for the purpose of recovery of a loan or debt, the purchase price shall computed as follows:

Conditions to be fulfilled for adopting the above valuation

-

Applicable to persons dealing in buying and selling of second hand goods

-

Input credit is not availed on purchase of the goods which are sold

-

second hand goods means used goods as such or after such minor processing which does not change the nature of the goods

Valuation of second hand goods sold other than by a dealer of such goods

In case of second hand goods sold other than by a dealer, the valuation of such supply shall be as per Section 15(1) of the CGST Act where the value of supply shall be the transaction value, which is the price actually paid or payable for the said supply, the supplier and the recipient of the supply being not related and the price is the sole consideration for the supply. However in respect of old and used motor vehicles, they can claim the benefit of reduced tax rate calculated on the marginal value as per Notification No. 8/2018-Central Tax(Rate) dated 25/01/2018.

Valuation in case input tax credit is availed

Valuation as per Rule 32(5) cant be adopted only for a dealer and only if input credit is not availed. Hence if input tax credit is availed, valuation shall be done as per Section 15(1) of the CGST Act where the value of supply shall be the transaction value, which is the price actually paid or payable for the said supply, the supplier and the recipient of the supply being not related and the price is the sole consideration for the supply. This shall apply equally for dealer as well as for a person other than a dealer.

Rate of GST of used goods

The rate of GST of used goods shall be at the rate notified vide Notification No. 1/2017-Central Tax (Rate). However, for second hand vehicles, a separate notification No. 08/2018-Central Tax(Rate) dated 25.01.2018 was issued.

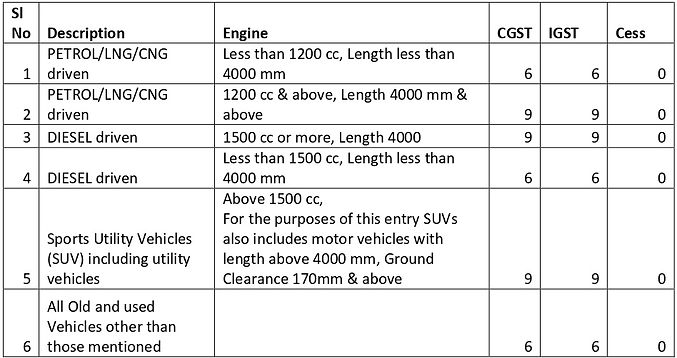

Rate of GST of used vehicles [Notification No. 08/2018-Central Tax(Rate) dated 25.01.2018]

NB:

-

For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under.

-

This rates shall apply only if the supplier of such goods has not availed input tax credit as defined in clause (63) of section 2 of the CGST Act, 2017, CENVAT as defined in CENVAT Credit Rules, 2004 or the input tax credit of Value Added Tax or any other taxes paid, on such goods.

-

Tax shall be calculated on the value that represents the margin of the supplier, on supply of such goods.

-

The value that represents the margin of the supplier shall be:

-

In case the dealer has claimed depreciation under section 32 of the Income Tax Act, 1961, the valuation of supply shall be as follows:

If the value so arrived is negative it shall be ignored

-

in any other case, the difference between the selling price and the purchase price and where such margin is negative, it shall be ignored.

GST liability in case input tax credit is availed

As per 18(6) of the CGST Act 2017, in case of supply of capital goods or plant and machinery, on which input tax credit has been taken, the registered person shall pay an amount which shall be higher of the following:

-

input tax credit taken on the said capital goods or plant and machinery reduced by five percentage points for every quarter or part thereof from the date of the invoice for such goods [Rule 40(2) of the CGST Rules 2017].

-

tax on the transaction value of such capital goods or plant and machinery determined under section 15.

Rule 44(6) of the CGST Rules 2017 also provides for the manner in which amount of input tax credit shall be determined for the purposes of sub-section (6) of section 18 in the case of capital goods. The calculation shall be as per clause (b) of sub-rule (1) of the said rule as shown below:

Input tax credit attributable to remaining useful life = Input tax credit taken X Remaining useful life of the capital goods/60

For example, ABC Ltd has sold a machinery costing Rs.250000 purchased on 08/12/2017 and on which input credit of Rs.45000 was availed to XYZ Ltd for Rs.90000 on 25/02/2020. Calculate GST liability.

GST liability shall be higher of the following:

-

Rs.45000- (5% of Rs.45000 for 13 quarters) => Rs.15750 [Rule 40(2) of the CGST Rules 2017].

-

GST @18% of Rs.90000 => Rs.16200

GST to be paid is Rs.16200

In the above calculation instead of Rule 40(2), calculation can be also be made as per Rule 44(6) as given below:

Input tax credit attributable to remaining useful life = 45000 X 21/60 => Rs.15750 which is same as that calculated under Rule 40(2) and hence the GST liability shall still be Rs.16200.

The amount shall be determined separately for input tax credit of central tax, State tax, Union territory tax and integrated tax. Provided that where the amount so determined is more than the tax determined on the transaction value of the capital goods, the amount determined shall form part of the output tax liability and the same shall be furnished in FORM GSTR-1.

As per proviso to section 18(6), where refractory bricks, moulds and dies, jigs and fixtures are supplied as scrap, the taxable person may pay tax on the transaction value of such goods determined under section 15.

Exemption from reverse tax for second hand goods

As per Section 9(4) of the CGST Act 2017, where taxable supply of goods or services or both are made by an unregistered supplier to a registered person, tax shall be paid by such registered person on reverse charge basis as the recipient and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both. For instance, if A an unregistered dealer is selling goods to B, a registered person, B shall, instead of paying tax to A as is normally done, pay the tax directly.

However vide Notification No.10/2017-Central Tax(Rate), Central Government has exempted a registered person, dealing in buying and selling of second hand goods from payment of tax on reverse charge basis on purchase from an unregistered supplier if the following conditions are satisfied:

-

Buyer is a registered supplier dealing in buying and selling of second hand goods

-

Buyer and seller are located in the same state

-

Goods being purchased are Second hand goods

-

Supplier is an unregistered person

-

The buyer is paying tax on supplies valued at sales price minus purchase price adopting Rule 32(5) of the CGST Rules 2017.

Tax treatment on used goods can be summarised in the table below:

.jpg)

Transactions deemed to be supply

Supply without consideration (Schedule I)

As per schedule I of CGST Act 2017, permanent transfer or disposal of business assets without any consideration where input tax credit has been availed shall be treated as supply. In such case the tax liability shall be computed as per Section 18(6) read with Rule 40(2) and 44(6) of the CGST Act, 2017.

For instance, Rahul has transferred his Personal Computer originally costing Rs.35000 plus tax of Rs.6300 purchased on 25/04/2017 and used for his business purpose to his brother without any consideration on 12/02/2020. He had claimed input tax on the asset. Hence this transfer shall be deemed to be supply as per Schedule I to the Act. Tax liability shall be computer as below:

As per 18(6) of the CGST Act 2017, the amount to be paid is higher of the following:

-

Tax on consideration which in ‘Nil’ in this case

-

No of quarters from the purchase date= 12

Tax as per Rule 40(2) = Rs.6300 minus 5% of Rs.6300 for 12 quarters = Rs.2520

The tax liability in this case is Rs.2520

Transfer of business assets deemed to be supply (Schedule II)

-

where goods forming part of the assets of a business are transferred or disposed of by or under the directions of the person carrying on the business so as no longer to form part of those assets, whether or not for a consideration, such transfer or disposal is a supply of goods by the person;

Here, the tax treatment shall be dependent on whether ITC was availed or not. If ITC was availed, then tax shall be calculated on transaction value at the rate as per Notification No. 1/2017-Central Tax (Rate) or amount calculated as per Section 18(6) read with rule 40(2) or 44(6) whichever is higher. If ITC was not availed, then tax shall be calculated on transaction value at the rate as per Notification No. 1/2017-Central Tax (Rate) except in the case of motor vehicles, where tax shall be calculated on marginal value as per Notification No. 8/2018-Central Tax (Rate).

-

where, by or under the direction of a person carrying on a business, goods held or used for the purposes of the business are put to any private use or are used, or made available to any person for use, for any purpose other than a purpose of the business, whether or not for a consideration, the usage or making available of suchgoods is a supply of services;

For instance, Ajay owner of Ajay Associates has given his Laptop which he was using for his business purpose to his son for his personal use during his study tour for 3 months. Usage of such Laptop is deemed to be a supply of services rendered by Ajay Associates for which they are liable to pay GST.

-

where any person ceases to be a taxable person, any goods forming part of the assets of any business carried on by him shall be deemed to be supplied by him in the course or furtherance of his business immediately before he ceases to be a taxable person, unless—

-

the business is transferred as a going concern to another person; or

-

the business is carried on by a personal representative who is deemed to be a taxable person.

-

For instance, Tony decided to quit his business and has ceased to be a taxable person. However he shall be deemed to have supplied all the goods forming part of his business on the date of termination of his business and liable to tax accordingly unless he has transferred his business as a going concern to another person or his business is carried on by a personal representative who is deemed to be a taxable person.

Page views: