Home->Resources->Income Tax->

Income chargeable under the head Salary

[Updated as on Mar 31, 2020]

As per section 15 of the Income Tax Act, 1961, following income shall be chargeable to income-tax under the head "Salaries"—

-

any salary due from an employer or a former employer to an assessee in the previous year, whether paid or not;

-

any salary paid or allowed to him in the previous year by or on behalf of an employer or a former employer though not due or before it became due to him; In such cases where any salary paid in advance is included in the total income of any person for any previous year it shall not be included again in the total income of the person when the salary becomes due.

-

any arrears of salary paid or allowed to him in the previous year by or on behalf of an employer or a former employer, if not charged to income-tax for any earlier previous year. In such cases, the assessee is entitled to relief under section 89(1).

However it may be noted that any salary, bonus, commission or remuneration, by whatever name called, due to, or received by, a partner of a firm from the firm shall not be regarded as "salary" for the purposes of this section.

Definition of Salary

Salary is defined under section 17(1) as follows:-

"salary" includes—

(i) wages;

(ii) any annuity or pension;

(iii) any gratuity;

(iv) any fees, commissions, perquisites or profits in lieu of or in addition to any salary or wages;

(v) any advance of salary;

(va) any payment received by an employee in respect of any period of leave not availed of by him;

(vi) the annual accretion to the balance at the credit of an employee participating in a recognised provident fund, to the extent to which it is chargeable to tax under rule 6 of Part A of the Fourth Schedule being;

-

contributions made by the employer in excess of ten per cent of the salary of the employee; and

-

interest credited on the balance to the credit of the employee in so far as it is allowed at a rate exceeding such rate as may be fixed by the Central Government in this behalf by notification in the Official Gazette.

(vii) the aggregate of all sums that are comprised in the transferred balance from a provident fund with existing balances upon recognition as referred to in sub-rule (2) of rule 11 of Part A of the Fourth Schedule of an employee participating in a recognised provident fund, to the extent to which it is chargeable to tax under sub-rule (4) thereof had the provisions of this part been in force from the date of the institution of such fund; and

(viii) the contribution made by the Central Government or any other employer in the previous year, to the account of an employee under a pension scheme referred to in section 80CCD;

Deduction from Salaries

As per Section 16 of the Income Tax Act, following are the deductions allowed while computing the income chargeable under the head salaries:

-

a deduction of fifty thousand rupees or the amount of the salary, whichever is less (16(ia));

-

a deduction in respect of any allowance in the nature of an entertainment allowance specifically granted by an employer to the assessee who is in receipt of a salary from the Government, a sum equal to one-fifth of his salary (exclusive of any allowance, benefit or other perquisite) or five thousand rupees, whichever is less (16(ii));;

-

a deduction of any sum paid by the assessee on account of a tax on employment within the meaning of clause (2) of article 276 of the Constitution, leviable by or under any law(16(iii));.

Relief under Section 89(1)

An assessee is entitled to relief under section 89(1) where he is in receipt of a sum in the nature of:

-

salary, being paid in arrears or in advance; or

-

salary for more than twelve months in any one financial year; or

-

a payment which under the provisions of clause (3) of section 17 is a profit in lieu of salary, or

-

family pension as defined in the Explanation to clause (iia) of section 57, being paid in arrears,

due to which his total income is assessed at a rate higher than that at which it would otherwise have been assessed. As per Rule 21AA of Income Tax Rules, where the assessee, being a Government servant or an employee in a [company, co-operative society, local authority, university, institution, association or body], is entitled to relief under sub-section (1) of section 89, he may furnish to the person responsible for making the payment referred to in sub-section (1) of section 192, the particulars specified in Form No. 10E. The form should also be filed online through the income tax e-filing portal along with the return of income.

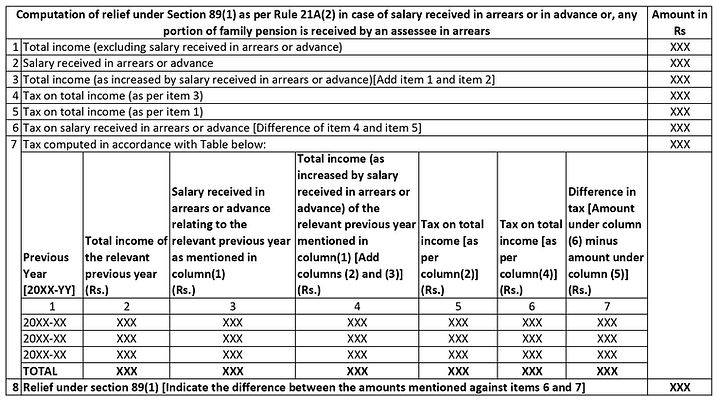

Computation of relief shall be as per Rule 21A(2) as shown below:

Illustration

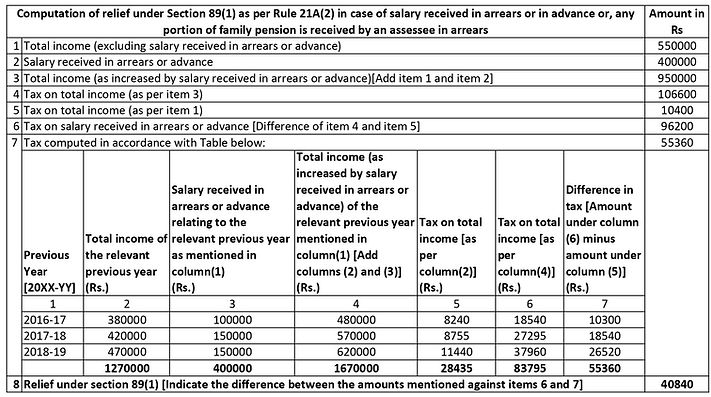

Mr.Gopal is in receipt of arrears of salary to the tune of Rs.450000 for the period from August 2016 to July 2019 yearwise break up of which is shown below. His total income computed for the FY 2019-20 including the arrear amount is Rs.950000. Compute his eligible relief under Section 89(1) for the FY 2019-20.

Break up of arrear received

FY Total income Tax paid Arrear received

2016-17 380000 8240 100000

2017-18 420000 8755 150000

2018-19 470000 49400 150000

2019-20 500000 50000

Here it is to be noted that the relief is to be calculated in respect of the salary amount received for the period prior to the relevant financial year for which relief is to be computed. Hence the amount of arrear received in respect of FY 2019-20 need not be considered as arrear but included as part of the total income of that year.

Therefore the total income for FY 2019-20 including arrears : Rs.950000

Amount of arrear received in respect of earlier years : Rs.400000

Total income excluding arrears : Rs.550000

Relief shall be computed as follows:

Mr.Gopal is thus eligible for a relief of Rs.40840 under section 89(1).

Page views: